GSTR3A Notice & Reply

Notice to return defaulter for not filling return

Ekatra Consulting

4/21/20231 min read

Introduction

GSTR-3A is not a return. The taxpayers registered under GST must file monthly, quarterly and annual returns as notified by the Central Board of Indirect Taxes and Customs (CBIC).

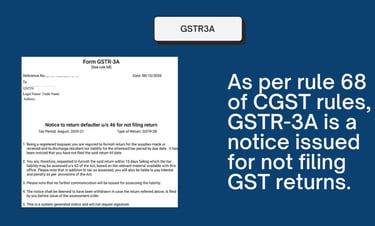

As per rule 68 of CGST rules, GSTR-3A is a notice for not filing GST returns issued under the GST regulations.

A notice in FORM GSTR-3A shall be issued, electronically, to a registered person who fails to furnish return under section 39 or section 44 or section 45 or section 52.

GSTR-3A is issued by the GST department when a taxpayer has not filed GST returns continuously.

What action need to be taken after receiving GSTR3A

When a taxpayer receives a notice under form GSTR 3A then the taxpayer has to file the return within 15 days from the date of notice along with penalty and late fees.

Time period to respond GSTR3A

After receiving a notice in Form GSTR-3A, the taxpayer must file return in Form GSTR-3B or any other return, as the case may be, within 15 days of issue of such notice and discharge the tax liability along with late fee and interest, if any.

How to respond to this GSTR3A notice?

If such a notice is received from the GST department, it is advisable for the taxpayer to immediately file any pending GST returns. If the GST returns are filed and any tax liability is cleared, there is no need to respond to GST 3A notice .

In case the taxpayer fails to file the pending return or fails respond to the above notice, GST registration could be cancelled and the show cause notice in FORM GSTR REG-17 would be issued.

Conclusion:

GSTR-3A is notice not a return. If you files pending GSTR3B and GSTR1 return withi 15 days there is no need to respond to GST 3A notice.

Click To Download the Notice Reply Format